The New York Times today reports that the US Attorney’s office in the District of Columbia has opened a criminal investigation into Fed Chairman Jerome Powell. Ostensibly and officially, the investigation is into the nature of the Federal Reserve’s renovation of its Washington headquarters, and whether or not Powell lied to Congress about the scope of the project. In the world of politics, stated reasons rarely match the actual reasons, however.

Corruption and mismanagement are always permissible in Washington so long as the guilty parties have friends in the administration. Powell was a Trump appointee in late 2017 but has since lost the president’s favor. If Trump’s public statements provide an accurate view into a reason for this, it’s that Powell has not been inflationist enough for Trump. Indeed, this is the most likely actual reason for the administration’s investigation into Powell.

After all, since before he was even sworn in for the current term, Trump has repeatedly and aggressively called for Powell and the Fed to force down interest rates. Although the Fed’s FOMC has repeatedly lowered the target interest rate since Trump was elected in November 2024, this apparently has not been enough for Trump who has demanded that the Fed cut the target policy rate even more.

Although the current investigation is said to be over renovation funds at the Fed, the investigation very conveniently provides some additional political pressure on Powell and the central bank, and may help yield even looser monetary policy to better suit Trump fondness for monetary inflation.

The Inflationist Fed Isn’t Inflationist Enough for Trump

Contrary to the myth pushed by the Fed and its supporters, the central bank does not ensure “price stability” nor is it a bulwark of any kind against monetary and price inflation. Rather central banks work to increase inflation for political purposes.

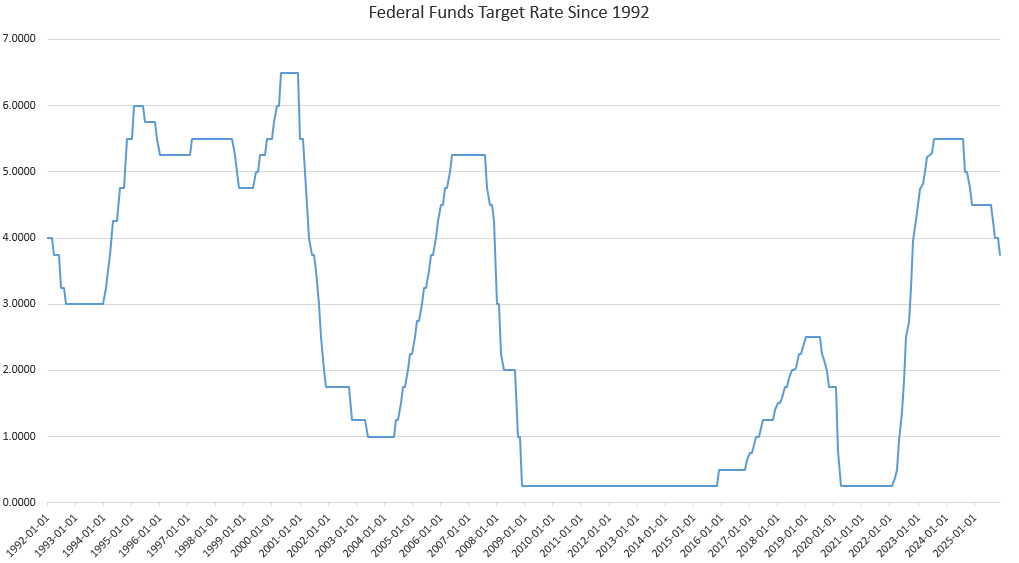

The US’s Federal Reserve is no different, and after a short period of relative monetary tightening to counter the 40-year high in price inflation during 2022, the Fed reverted to an easy money stance in late 2024. At the time, the Fed began to once again embrace monetary inflation to help push down interest rates.

Specifically, the current cycle of Fed rate cuts began in September 2024. Although one could claim that was to create stimulus for the Biden economy, it is nonetheless also true that the FOMC and Powell continued to cut the target rate after Trump was elected. The FOMC cut the target rate in November (after the election) and again in December. The Fed then cut the target rate in September 2025 and again in November 2025. In all, the FOMC cut the target rate by 125 basis points since Trump’s election.

Consequently, the target policy rate is back down to the lowest level since October of 2022. This is not a Fed that is doubling down on high interest rates.

The Fed’s loose stance on easy money can be seen in continued price inflation. The core CPI inflation rate in November 2025 was 2.6 percent, well above the Fed’s two-percent inflation target. Moreover, the most recent PCE measure, from September 2025 was 2.8 percent, and the Cleveland Fed’s nowcast for December 2025 is 2.6 percent. The fact that the Fed continues to cut its policy rate as price inflation remains above the target price-inflation rate shows that the Fed is choosing to favor further monetary expansion.

Given the current realities of price inflation, interest rates are too low, rather than too high. This is true even by conventional logic. (The more correct view is that the price inflation rate “target” should not be two percent but should be zero or even below zero (thanks to technological progress and productivity gains).

Note, also, that the Fed has continued to monetize debt with its continued purchases of federal Treasurys. This adds additional monetary ease to the open market operations used to manipulate interest rates downward. In other words, there is plenty of Fed-fueled monetary inflation going on.

Yet, the administration would have us believe that the central bank is filled with intransigent hard-money men who are holding interest rates unnecessarily high in order to make Trump look bad. There is nothing “hard-money” about the Fed, but even the Fed’s continued embrace of artificially low interest rates is not enough for the White House. Trump wants even lower interest rates and even more quantitative easing.

So let’s be clear: the conflict here is not between one side that wants “sound money” and another side that wants inflation. Both sides push more inflation continually, although one side (the White House) at the moment appears to want a more inflation than the other side (the Fed).

The Fed’s Myth of Independence

The White House’s investigation of Powell has prompted the Fed and its supporters to invoke the old myth of Fed Independence from federal policymakers. This old canard is built on the idea that the central bank is a nonpolitical institutions that makes its decisions based on the most objective economic analysis, free from political intervention.

For example, upon hearing of the administration’s investigation, the Federal Reserve published a short video response from Jerome Powell stating:

The threat of criminal charges is a consequence of the Federal Reserve setting interest rates based on our best assessment of what will serve the public, rather than following the preferences of the president. ... This is about whether the Fed will be able to continue to set interest rates based on evidence and economic conditions — or whether instead monetary policy will be directed by political pressure or intimidation.

Now, Powell is almost certainly right that the real motivation behind the investigation is an effort to pressure the Fed into lower interest rates and more monetary inflation.

Video message from Federal Reserve Chair Jerome H. Powell: https://t.co/5dfrkByGyX pic.twitter.com/O4ecNaYaGH

— Federal Reserve (@federalreserve) January 12, 2026

Other parts of the statement are, frankly, absurd. For instance, Powell attempts to draw a contrast between the Fed and the administration by claiming that the Fed sets interest rates “based on evidence and economic conditions” and an assessment of “what will serve the public.”

The Fed is many things, but a servant of the common man or “the public” is not one of them. Central banks exist to keep borrowing costs low for governments, and to augment government revenue by extracting more wealth from the population in the form of the inflation tax. The idea that central bankers pore over economic reports to dispassionately determine the “best” policy for “the public” is pure propaganda.

Historically, the idea that the Fed is an apolitical data-driven institution has been disproven so many times it’s difficult to keep count. Over the past century, there are countless cases of the Fed explicitly working to facilitate wartime spending and welfare-state spending by monetizing the federal debt. More recently, in the wake of the Great Recession, the Fed bought up trillions of dollars worth of mortgage-backed securities to bail out billionaire bankers. The Fed now holds trillions in government securities to assist politicians with even more deficit spending, even as the total national debt approaches $40 trillion.

Nor is the Fed even independent in theory, given that statute makes it clear that the Fed answers to Congress. The last I checked few institutions created and overseen by Congress are nonpolitical.

Moreover, even if it were true that the Fed is data-driven, it’s clear that the Fed isn’t very good at following the data. Take, for example, the Fed’s decision to lower the target interest rate in September of 2024, right before the election. The Fed at the time claimed that the decision was justified by “the data” which showed the CPI inflation rate rapidly returning to the 2 percent target. Now, more than fifteen months later, the Fed’s data-driven prediction still hasn’t come true. The PCE inflation rate (as well as the CPI inflation rate) is higher now than it was in late 2024.

Moreover, the past few months have made it very clear that the Fed is just winging it when it comes to data. This can be seen in how the FOMC was making policy at the same time the federal inflation data and employment data was either partial, delayed, or nonexistent during the federal shutdown during fall of 2025. Even as it was flying blind for this period, the FOMC still met and decided to further reduce the target rate. How could the Fed make these decisions without the very data the Fed claims guides policy? The answer is simple: these were political decisions.

So, what we have in this conflict between Trump and Powell is little more than two factions within the Federal government fighting over how exactly to use the Fed’s many powers to inflate, exploit, and help fund an ever expanding federal government. Neither party has any interest in sound money, honest economic policy, or limits on federal power. Moreover, with Trump, one can never discount the possibility that the whole feud stems from some perceived personal slight by Powell against Trump. Anything is possible, except, of course, actual Fed “data-driven independence” That has never existed and never will.